Provo Water Damage Insurance Claims: Vital Questions for Your Agent

Discovering standing water in your basement in Orem or a ceiling leak in your Lehi home is a high-stress event. In the aftermath of a pipe burst or a faulty appliance, most Utah County homeowners immediately think of two things: getting the water out and calling their insurance agent. However, navigating the intersection of insurance policies and professional restoration services requires more than just a cursory phone call.

Utah’s unique climate—ranging from heavy spring runoff in Alpine to sudden summer "monsoons" in Santaquin—creates various scenarios for home water damage. Understanding the specifics of your policy is the difference between a fully covered restoration and an out-of-pocket financial disaster. When you find yourself searching for reliable local house restoration services, you must be prepared to have a detailed, technical conversation with your insurance representative.

1. Identifying Your Coverage Type: "Is This a Covered Peril?"

The first question you must ask is simple but critical: "Based on the source of this water, is this a covered peril under my specific policy?" Not all water damage is created equal in the eyes of an insurance adjuster in Provo or Spanish Fork. Standard homeowners insurance typically covers "sudden and accidental" water discharge, such as a water heater failing in an American Fork rambler. However, gradual damage—like a slow leak behind a shower wall that has been occurring for months—is often denied. You need to clarify if your policy includes:

·Sudden Pipe Bursts: Common in Eagle Mountain during deep winter freezes. Appliance Overflows: Dishwashers or washing machines.

·Sewer Backup: Usually requires a specific "Sewer and Drain Backup" rider.

·Overland Flooding: Standard policies rarely cover water entering from the ground up; this requires NFIP or private flood insurance.

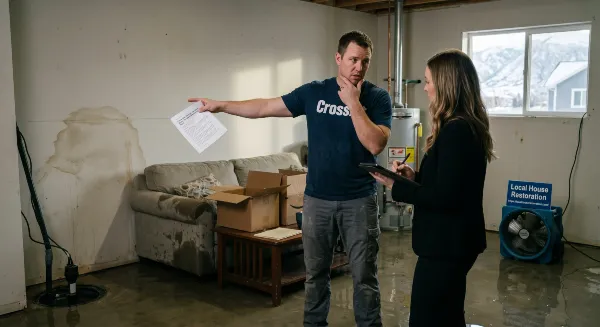

2. The "Right to Choose" Your Restoration Professional

Insurance companies often have "preferred vendors" or "program contractors." When you call your agent, they may suggest a specific franchise. A vital question to ask is: "Do I have the right to select my own restoration company, or am I required to use your preferred vendor list?" In the state of Utah, homeowners generally have the right to choose their own contractor. Using a local house restoration expert who understands the specific building codes in Lindon or Pleasant Grove ensures that the person working on your home answerable to you, not just the insurance company. Ask your agent if choosing an outside contractor will affect the claims process or the "guarantee" of the work. Pro-Tip for Utah County Residents Many neighborhoods in Saratoga Springs and Vineyard are newer builds. Ask your agent if your policy covers "Ordinance or Law" changes. If the restoration requires bringing your home up to the current 2026 building codes, you want to ensure the insurance covers those additional costs.

3. Clarifying Your Deductible and Coverage Limits

Before the extraction fans start running in your Springville home, you need to know your financial exposure. Ask: "What is my specific deductible for a water damage claim, and are there sub-limits for certain types of damage?" Sometimes, a policy might have a $1,000 deductible for standard claims but a separate, higher deductible for wind/hail or flood. Furthermore, some policies have "sub-limits" on mold remediation. For instance, your policy might cover $50,000 in water damage but only $5,000 for "fungi, wet or dry rot, or bacteria." In the humid aftermath of a basement flood in Mapleton, mold can develop quickly, and $5,000 may not cover professional remediation.

4. Ask About "Actual Cash Value" vs. "Replacement Cost"

This is where many Utah County residents get caught off guard. Ask your agent: "Is my dwelling and personal property coverage based on Replacement Cost Value (RCV) or Actual Cash Value (ACV)?"

·RCV: Pays to replace your damaged items with new ones of similar kind and quality.

·ACV: Pays what the item was worth at the time of loss, accounting for depreciation.

If your 10-year-old finished basement in Highland is destroyed, an ACV policy will pay significantly less than it costs to actually rebuild it today.

5. Documentation and Mitigation Requirements

Insurance policies contain a clause regarding the "duty to mitigate." This means the homeowner must take reasonable steps to prevent further damage. Ask your agent: "What specific documentation (photos, moisture readings, logs) do you require from my restoration company to ensure the claim is processed smoothly?" Professional restoration teams in Payson and Elk Ridge should provide "daily moisture logs." These logs prove to the insurance company that the home was dried to industry standards. If you don't ask what the insurance company needs, you might find your claim stalled because of "insufficient proof of dry-down."

6. Understanding "Additional Living Expenses" (ALE)

If the water damage in your Cedar Hills home is extensive—perhaps a category 3 "black water" event from a sewage backup—you may not be able to live in the house during the dry-out and reconstruction. Ask: "Does my policy include ALE, and what are the daily or total limits?" ALE covers the cost of hotels, meals, and even increased mileage if you have to move further away from your work or schools in Utah County. Knowing these limits early helps you plan whether you can stay in a local Marriott or if you need to find a short-term rental.

Keywords for Your Insurance Search

When researching your situation online, use these keyword phrases to find relevant Utah-specific insurance information:

·Utah homeowners insurance water damage coverage limits

·How to file a water damage claim in Provo UT

·Sewer backup vs flood insurance Utah County

·Restoration company insurance billing Salt Lake/Utah County

·Water damage mitigation requirements for insurance

Conclusion: Being Your Own Best Advocate

Water damage doesn't just threaten the structural integrity of your home in Salem or Goshen; it threatens your financial peace of mind. By asking these targeted questions, you move from a passive participant to an informed advocate for your property. Always remember that while the insurance company pays the bill, the restoration company works for you. Partnering with a local house restoration professional who is experienced in navigating the Utah insurance landscape is the most effective way to ensure your home is returned to its pre-loss condition—or better.

Serving all of Utah County: Provo, Orem, Lehi, American Fork, Spanish Fork, Springville, Saratoga Springs, Eagle Mountain, Cedar Hills, and surrounding areas